Use Wozber and land your dream job

Create CV

No registration required

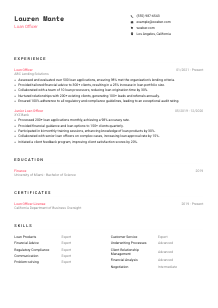

Navigating financial pathways, but your CV seems to need a loan? Check out this Loan Officer CV example, created with Wozber free CV builder. Learn how to present your lending expertise in line with job requirements, ensuring your career investments pay off with interest!

Loan officers are trusted with decisions that affect both portfolio quality and client outcomes. A CV for this work has to show more than sales energy or banking experience alone. It needs to make your lending judgment visible through the kinds of files you handled, the loan guidance you gave, and the way you worked within underwriting standards and regulatory requirements.

Early CV screening for loan officer roles often turns on whether your background clearly connects client-facing origination work with compliant execution. Wozber's free CV builder helps you tailor that connection into an ATS-compliant CV by aligning your wording with the posting's loan products, underwriting, and licensing language, so hiring teams can quickly see where you fit in the origination process.

This section is brief, but it still answers practical hiring questions. For a Loan Officer, that usually means confirming who you are, how to reach you, whether your title matches the function, and whether you meet basic location expectations when the employer needs someone local.

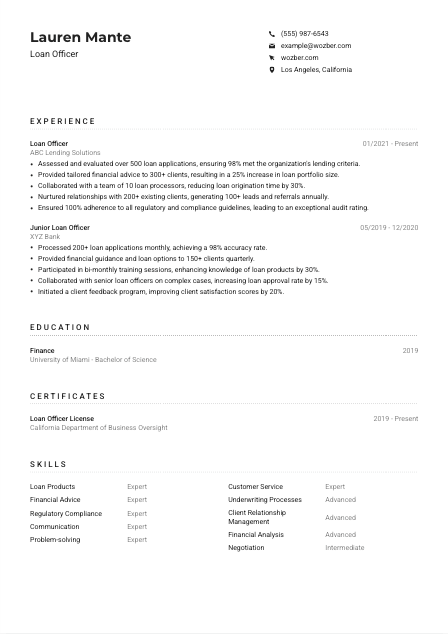

Use your full name in a clear, readable style so it is easy to identify at a glance. In finance and lending roles, a clean presentation supports the professional tone you want before the reader gets to your production history, client portfolio, or compliance record.

Place "Loan Officer" directly below your name when that is the role you are pursuing. Matching the posted title helps frame the rest of your CV around loan origination, client advising, underwriting coordination, and relationship development rather than broader banking work that may be less relevant.

Your contact details should remove friction for recruiters, branch leaders, or lending managers who may want to schedule a call quickly after reviewing your experience.

If the posting requires local presence, state your city and state clearly. In the example, "Los Angeles, California" directly supports a location-specific requirement and saves the employer from wondering about relocation or licensing logistics.

Include a LinkedIn profile or professional website only if it strengthens your candidacy. For loan officers, that might mean a polished profile showing lending experience, licenses, banking employers, or business development credibility that matches the CV.

Keep this section simple, accurate, and aligned with the posting. It should confirm that you are reachable, locally viable when required, and already positioned for loan officer work.

Experience is where hiring teams look for proof that you can move from application review to funded loan while managing client expectations and internal handoffs. The strongest entries show lending scope, production or service outcomes, and how you handled compliance, processors, and underwriters along the way.

Read the posting for the operational language behind the title. For this role, that includes assessing loan applications, advising clients on suitable terms, collaborating with processors and underwriters, generating leads and referrals, and staying within regulatory guidelines. Those phrases tell you what your bullets need to demonstrate through real lending work, not general customer service.

List your most recent lending or banking position first, followed by earlier roles. Include employer, title, and dates so the reader can quickly see your progression from junior processing or support work into more independent loan officer responsibility.

Each bullet should show what you handled and what changed because of your work. Replace generic statements like "helped clients with loans" with specifics such as application volume, loan product guidance, approval support, turnaround time, portfolio growth, referral generation, or audit performance. In the example, bullets about evaluating 500+ applications and advising 300+ clients work because they connect core responsibilities to measurable lending outcomes.

Use numbers that make sense in loan origination and banking. That can include file volume, accuracy rate, approval rate, cycle-time reduction, client count, portfolio growth, referrals, or compliance performance. A metric like reducing origination time by 30% says far more about how you work with processors and underwriters than a broad claim about being efficient.

Do not crowd this section with unrelated branch tasks or general office work if you have stronger lending material. Prioritise bullets that show product knowledge, underwriting familiarity, financial guidance, client retention, and regulatory discipline. Every line should help the employer picture you handling their pipeline and borrower relationships.

A hiring manager should be able to scan your experience and understand your loan volume, client work, internal coordination, and compliance habits. If those four areas are visible, your experience section is doing its job.

Education matters in lending because it gives context to your financial judgment and product knowledge. It will not outweigh strong production experience, but it does help confirm that you have the business, finance, or analytical foundation the role calls for.

When the posting asks for a bachelor's degree in Finance, Business Administration, or a related field, make that match easy to spot. If your degree is directly relevant, as with a Bachelor of Science in Finance, spell out the degree and field clearly so the connection is immediate.

List degree, field of study, school, and graduation year in a consistent format. This is enough for most loan officer CVs and gives recruiters the information they need without forcing them to search for basic qualification details.

If your education aligns closely with lending, move that relevance to the surface. Finance, accounting, business administration, risk analysis, or real estate coursework can reinforce your readiness for work involving borrower evaluation and loan terms.

Relevant coursework can help early-career candidates or career changers. Classes in commercial banking, credit analysis, financial law, consumer finance, or risk management can support your CV when your lending experience is still growing.

Honors, finance society involvement, case competitions, or capstone projects are worth listing if they strengthen your profile. Keep the additions selective and tied to analytical work, business judgment, or financial services interest rather than filling space.

Your education section should confirm that you meet the academic requirement and support your lending background. Once that is clear, let your experience carry the heavier weight.

Credentials carry real weight in loan origination because they can affect eligibility to perform the work. This section should make required licenses easy to find and show that you stay current in a field shaped by regulation, policy changes, and product-specific rules.

Start with any credential the posting specifically requests. For many loan officer openings, that means a valid state-specific license. If you hold the exact license relevant to the role, place it first so there is no ambiguity about your eligibility.

List the licenses and certifications that directly support lending, compliance, mortgage or consumer loan work, and client advising before broader professional development items. The CV example does this well by featuring the California Loan Officer License instead of burying it under less important training.

Include issue dates, renewal windows, or active date ranges when a credential must remain current. In regulated financial roles, date visibility matters because employers need to know whether your license status supports immediate hiring.

If you have recent training in underwriting updates, lending regulations, fair lending practices, loan products, or compliance refreshers, include it when relevant. It shows you keep pace with the rules and market conditions that affect borrower guidance and file quality.

This section should quickly answer two questions. Are you licensed for the work, and are your credentials current enough to step into the role without delay?

A loan officer skills section works best when it mirrors the actual mix of lending knowledge, client communication, and process coordination used on the job. Generic business skills are not enough on their own. Hiring teams want to see the tools of the role, from loan products and underwriting awareness to relationship management and regulatory discipline.

Start with the posting and identify the skills tied to daily work. Here, the important ones include loan products, underwriting processes, regulatory guidelines, client communication, interpersonal effectiveness, and financial guidance. Those are the skills that shape borrower conversations and file decisions.

Use the same terminology the employer uses when it accurately reflects your background. If the posting says "underwriting processes" and "regulatory guidelines," use those phrases instead of looser alternatives. In the example, skills such as Loan Products, Financial Advice, Regulatory Compliance, and Underwriting Processes align closely with the job description.

Choose the skills most relevant to loan origination and approval support instead of listing every capability you have developed in banking. A shorter list built around lending analysis, borrower communication, compliance, relationship management, and negotiation will read stronger than a long mixed list with weak relevance.

Your skills section should sound like the toolkit of a working loan officer. If the list supports application review, borrower advising, pipeline coordination, and compliance, it is on target.

Language ability matters in lending when it improves client conversations, document clarity, and relationship building. This section should be straightforward, with proficiency levels that reflect how well you can actually explain terms, gather information, and respond to borrower questions.

If the posting asks for fluent English verbally and in writing, state your English level clearly. Use a label such as "Native" or "Fluent" so there is no uncertainty about your ability to handle client discussions, written communication, and loan documentation.

Put the required language first, then add others that may support the market you serve. For some loan officer roles, an additional language can help with community outreach, referral business, and smoother borrower communication, but it should not distract from the core requirement.

Stick to standard levels such as Native, Fluent, Intermediate, or Basic. Vague descriptions make it harder for employers to judge whether you can manage real borrower interactions or only hold casual conversation.

Additional languages can be especially useful in regions with diverse borrower populations or high-touch relationship banking. In the example, Spanish strengthens the profile because it suggests broader client access, but the main point remains clear English fluency for the role's written and verbal demands.

Only claim a level you can support in a real lending conversation. If you may need to explain loan terms, gather financial details, or respond to objections in that language, your rating should reflect that reality.

For loan officer roles, language proficiency is valuable when it improves client service and communication quality. Keep the section clear enough that the employer knows exactly how you can operate with borrowers and colleagues.

Your summary sits at the top of the CV, so it should quickly establish the kind of lending professional you are. A few lines can cover your experience level, the parts of the loan process you handle well, and the results or strengths that make your profile worth a closer look.

Before writing, identify the essentials of the target position. For a loan officer, that usually means evaluating applications, guiding borrowers to suitable loan options, coordinating with processors and underwriters, building referral-producing relationships, and staying inside regulatory requirements. Your summary should reflect that mix, not a generic banking profile.

Begin with your title and relevant years of experience. A line such as "Loan Officer with 3+ years of experience in loan application review and client financial guidance" immediately gives the reader a usable frame for the rest of the CV.

Choose two or three high-value points that align with the employer's needs. That could be growth in loan portfolio size, strong application accuracy, experience with underwriting coordination, referral generation, or a consistent compliance record. The example summary works because it ties experience to portfolio growth, collaboration, and regulatory discipline instead of staying vague.

Aim for a short paragraph with concrete language. You do not need to cover every loan product or every achievement here. Give enough detail to establish your lending profile, then let the experience section provide the numbers and fuller context.

A good summary gives the reader a fast, accurate picture of your lending background and operating strengths. When it is tailored well, the rest of the CV feels consistent and easier to trust.

A Loan Officer CV works when it shows how you evaluate borrowers, guide clients toward suitable products, move files through origination, and stay compliant while doing it. That is the combination hiring teams need to see, whether they are filling a high-volume consumer lending role or a more relationship-driven banking position.

Use Wozber's free CV builder to organise that experience into an ATS-friendly CV format, then refine it with the ATS CV scanner so the language reflects the posting's lending, underwriting, and licensing requirements. The finished CV should make one thing clear right away: you can handle both the client side and the credit side of the job.