Use Wozber and land your dream job

Create Resume

No registration required

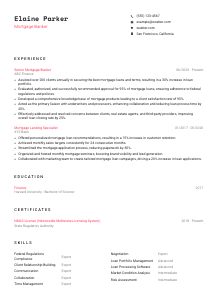

Crafting home loans, but your resume is feeling underwater? Check out this Mortgage Banker resume example, created with Wozber free resume builder. Learn how to align your lending expertise with job specifics, making your career just as solid as the foundations you finance!

Mortgage banking sits at the intersection of sales, credit judgment, and regulation. Hiring teams want to see more than loan volume. They need proof that you can guide borrowers through complex decisions, keep files moving with underwriters and processors, and stay disciplined around federal lending requirements while protecting the client experience.

A tailored resume changes how quickly that picture comes into focus. When your experience uses the same lending language as the posting, an ATS-compliant resume is far more likely to surface the right strengths early, especially with Wozber's free resume builder helping you align titles, keywords, and mortgage-specific achievements. That makes it easier to recognize whether you can manage the full path from application to closing.

This section should confirm the basics a mortgage employer checks first: who you are, how to reach you, and whether any logistical requirement could slow the hiring process.

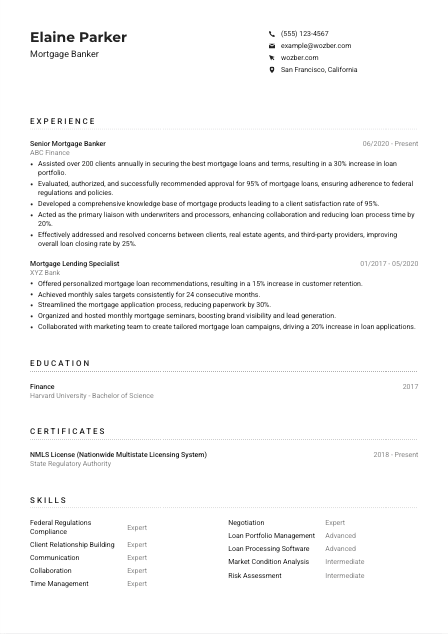

Use your full name as the most prominent text on the page. Mortgage banking is a client-facing profession, so your resume should read like professional business communication from the first line. Keep the formatting clean and easy to scan.

Place "Mortgage Banker" below your name if that is the role you are targeting. This helps frame your background immediately, especially if your previous titles include nearby variations such as Mortgage Lending Specialist or Loan Officer. When the target title is close to your actual work, mirroring it helps both recruiters and ATS systems sort your resume correctly.

Include a reliable phone number and a professional email address. In this field, first contact often leads to a screening call about licensing, production history, or market coverage, so accuracy matters. Check every character. A missed digit or outdated email can cost you an interview.

If the employer wants someone based in a specific market, show your city and state. Here, listing San Francisco, California directly answers a stated requirement and removes doubt about availability. If you are relocating, make that clear in a simple way rather than leaving the employer to guess.

A LinkedIn profile or professional website can support your resume when it reflects the same employment dates, titles, and licensing information. For mortgage bankers, consistency matters because hiring teams often compare your resume against your public profile for production credibility and career progression.

Your personal details should remove friction, not add it. When the title, contact information, and location are accurate and aligned with the opening, the employer can move straight to your lending background.

Experience carries the most weight in a mortgage banker resume because it shows how you perform in live production environments. Employers want to see client advisory work, loan evaluation, regulatory discipline, and cross-functional coordination reflected in actual results.

Start by pulling out the responsibilities that define the job. In this case, that includes helping clients secure the right loan terms, evaluating or recommending approvals, staying current on mortgage products and market conditions, and coordinating with underwriters, processors, agents, and third-party providers. Your experience bullets should answer those points with concrete examples from your own pipeline.

List positions in reverse chronological order, and make the strongest mortgage-lending experience do the most work. If you have held titles such as Senior Mortgage Banker or Mortgage Lending Specialist, those roles should clearly show client consultation, loan structuring, and file movement from application through closing. The sample resume does this well by leading with a role that handled both borrower guidance and approval recommendations.

Numbers matter in mortgage banking because they show scale and consistency. Include metrics such as annual client volume, portfolio growth, approval rate, pull-through rate, turnaround time, closing rate, retention, or sales target performance. The example metrics, like assisting over 200 clients annually, reducing process time by 20%, and improving closing rate by 25%, work because they connect daily lending work to business results.

Cut generic statements that could belong to any sales or finance role. Prioritize bullets that show mortgage-specific activity such as recommending products based on borrower goals, reviewing financial information, maintaining compliance with federal regulations, resolving document or processing issues, or coordinating with underwriting to keep conditions on track. Relevance matters more than listing every task you have ever handled.

Your work history should show how responsibility expanded over time. Maybe you moved from supporting applications to owning a larger client book, handling more complex loan scenarios, or improving process flow across teams. The transition from Mortgage Lending Specialist to Senior Mortgage Banker in the sample is a good illustration of growth because the later role carries broader client volume, stronger operational coordination, and larger performance outcomes.

By the end of your experience section, an employer should understand the kind of mortgage business you have handled, how well you move loans through the pipeline, and how reliably you balance client service with lending discipline.

Education matters here because many mortgage banking roles still screen for a bachelor's degree, especially when the work involves financial analysis, client advising, and regulatory awareness. Keep the section straightforward and relevant.

If the posting asks for a bachelor's degree in Finance, Business, or a related field, make sure that information is easy to find. A degree in Finance directly supports mortgage work because it signals familiarity with lending concepts, risk, and borrower financial evaluation.

List your degree, field of study, school, and graduation year or date in a consistent order. For example, "Bachelor of Science, Finance" gives hiring teams the information they need without extra clutter. Mortgage employers rarely need a long academic narrative unless you are very early in your career.

When your education aligns with the role, you do not need to oversell it. A finance degree from a recognized university already supports your case for a mortgage banking position. In the sample, the Bachelor of Science in Finance fits the requirement directly and reinforces the candidate's lending background without needing extra explanation.

If you are newer to the field, relevant coursework in finance, real estate, banking, credit analysis, or business law can strengthen this section. The same goes for finance clubs, case competitions, or research tied to lending or markets. If you already have several years of mortgage experience, keep these details brief or leave them out.

Academic honors, scholarships, or strong distinctions can be useful, especially for early-career candidates or competitive programs. Keep them if they add credibility. Skip them if they distract from stronger evidence in your lending experience and licensing.

For an experienced mortgage banker, education confirms the baseline qualification. It should support the story, not compete with the sections that show how you perform with borrowers, loan files, and compliance requirements.

In mortgage banking, this section can decide whether your application moves forward at all. Required licenses and current credentials should be easy to find and impossible to misread.

If the role requires an active NMLS license, list it at the top of this section with the full name and current status. That is a hard-screen item for many employers. In this posting, it is essential, so it should never be buried under unrelated certificates.

Only include certifications that strengthen your mortgage profile. Licensing, compliance, underwriting, financial counseling, or specialized lending credentials are worth keeping. General certificates that do not support mortgage production, regulation, or borrower advising can be left off.

Include the issue date and, when relevant, the active range. For licenses, current status matters as much as original issuance. The sample's "2018 - Present" format works well because it quickly shows continuity and active standing.

Mortgage banking changes with rate environments, investor overlays, and regulatory expectations. If you complete continuing education or hold additional role-relevant credentials, include them when they show you stay current with the lending landscape and compliance obligations.

A mortgage employer should be able to confirm your licensing position within seconds. Lead with the credentials that qualify you to originate, advise, or approve within the role's scope.

The skills section should read like the operating toolkit of a mortgage banker. Focus on abilities that affect borrower guidance, compliance, loan movement, and production performance.

Read the job description for the skill themes behind the responsibilities. Here, the clear priorities are federal regulations knowledge, client relationship management, communication, mortgage product knowledge, collaboration with underwriters and processors, and the judgment to evaluate or recommend loan approvals. Those are the skills your list should foreground.

Use the same terminology the employer uses when it reflects your real background. If the posting stresses "federal regulations" and "client relationships," use those exact ideas rather than replacing them with vague alternatives. The sample skills section mirrors this well with entries such as Federal Regulations Compliance, Client Relationship Building, and Market Condition Analysis.

Do not overload this section with every soft skill you have. Put the most job-relevant capabilities first, then support them in your experience bullets. A shorter list that includes mortgage compliance, borrower communication, loan portfolio management, risk assessment, and loan processing software is usually stronger than a long list of generic workplace traits.

Your skill list should sound credible to a mortgage hiring manager. If each item connects to loan production, borrower service, or lending compliance, the section is doing its job.

Language ability matters in mortgage banking because the work depends on clear conversations about rates, terms, documentation, timelines, and conditions. List only languages you can use confidently in a professional setting.

If strong English proficiency is listed, put English first and state your level clearly. Mortgage bankers spend much of their day explaining products, collecting financial details, and coordinating next steps, so this requirement is directly tied to daily performance.

Additional languages can strengthen your profile, especially in markets with diverse borrower populations. They are particularly useful when your work includes relationship building, community outreach, or helping first-time buyers navigate a complex lending process. Spanish in the sample is a good example of a second language that could widen client reach.

Terms like Native, Fluent, Professional, or Intermediate give more hiring value than vague descriptions. Be honest. If a language appears on your resume, an interviewer may test whether you can discuss financial topics and borrower communication in it.

Only include languages that could realistically support your work. Mortgage banking is detail-heavy, and misunderstandings around documentation or terms can create real risk, so professional usability matters more than casual familiarity.

Some locations benefit from multilingual client coverage more than others, but it is still a bonus rather than a universal requirement unless the employer says otherwise. Use language skills to expand your profile, not to distract from your lending record and licensing.

When language proficiency is presented clearly, it adds another layer of trust. Employers can quickly see whether you can communicate effectively with the borrower base they serve.

Your summary should capture the commercial and regulatory side of your background in a few lines. It needs to tell an employer what kind of mortgage banker you are, how much lending experience you bring, and what results or strengths define your work.

Before writing, identify the two or three themes that matter most in the posting. For this opening, those themes are borrower guidance, mortgage lending or underwriting experience, regulatory knowledge, and smooth coordination across the loan process. Your summary should bring those threads together quickly.

Begin with a direct line that states who you are professionally and how long you have worked in mortgage lending. A phrase like "Mortgage Banker with over 6 years in mortgage lending" works because it gives immediate context without wasting space.

Use the next sentence or two to mention strengths tied to the job, such as helping clients secure suitable loan terms, maintaining compliance with federal lending rules, improving process speed, or supporting strong closing outcomes. The sample summary succeeds because it combines client relationship work, regulatory discipline, and measurable operational improvement.

Aim for 3 to 5 lines with concrete language. Avoid broad claims like "results-driven professional" unless you immediately support them with mortgage-specific proof. This section should sound like a lender who understands borrowers, loan files, and production pressure, not a generic finance candidate.

A well-written summary should make the rest of the resume easier to read. In a few lines, it should establish your mortgage background, your operating strengths, and the kind of contribution you can make in a lending team.

Once each section reflects real lending work, current licensing, and measurable results, your resume becomes much easier to trust. That matters in mortgage banking, where employers need people who can win client confidence, manage loan flow, and stay aligned with regulation.

Use Wozber's AI resume builder and ATS optimization tools to tighten wording, align your experience with the job description, and present everything in an ATS-friendly resume format. The finished resume should make one thing clear right away: you can guide mortgage business from borrower conversation to closing with sound judgment.